Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

Although we will publish individual indicators on Friday, April 3, 2026, markets will be closed in observance of Good Friday. As a result, we will not be releasing our Weekly Economics next week. This makes the upcoming slew of data particularly important for markets, as investors digest the first measurable economic signals following the latest geopolitical shock. Next week’s releases should help clarify whether recent volatility remains contained or begins to translate into weaker fundamentals.

From a macro perspective, the US economy still enters this period from a position of relative strength. Investment spending remains well supported by the Inflation Reduction and CHIPS acts as well as by continued momentum related to artificial intelligence (AI) deployment, which has helped anchor growth and offset potential downside pressures. Financial conditions, while tighter than in prior cycles, have not yet derailed activity. However, the distribution of that resilience remains uneven. Roughly 10% of households continue to drive about half of total consumption, a dynamic that markets have increasingly internalized through strong equity performance and elevated asset prices. Unlike prior expansions, this cycle has leaned far more on financial wealth accumulation than on broad-based income or employment growth, leaving consumption – and market sentiment – more exposed to asset price swings.

For markets, this means that the current macro equilibrium remains highly sensitive to equity performance. As long as stock prices avoid a sharp and sustained correction, headline growth is likely to hold up reasonably well.

By contrast, for households dependent on wages and employment, rising petroleum prices represent a clear headwind. Higher gasoline prices tighten household cash flow and raise the risk of demand softness as discretionary spending adjusts. In the near term, we expect larger tax refunds tied to the One Big Beautiful Bill Act (OBBBA) to provide some cushioning, limiting immediate downside risk to consumption. That support, however, should be viewed as temporary rather than structural.

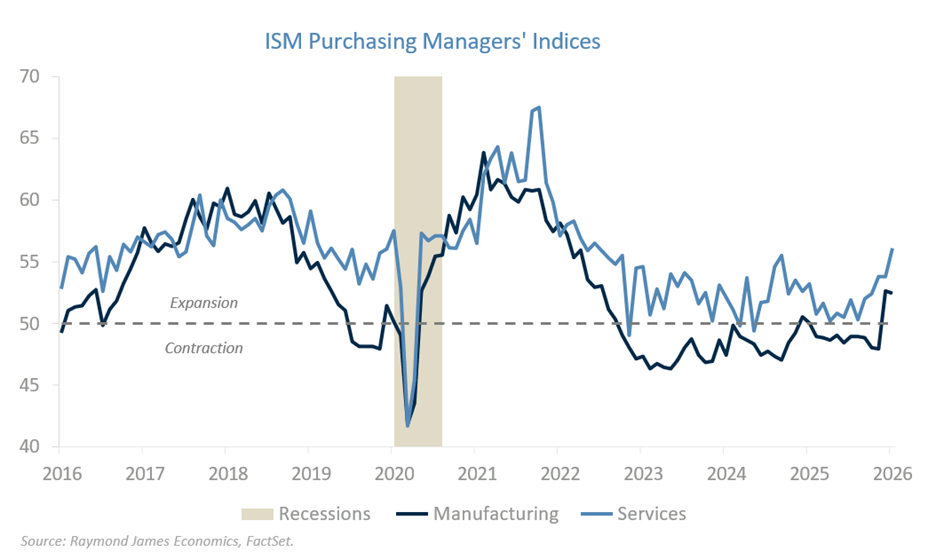

Against this backdrop, the ISM Manufacturing and Services PMIs will be key market inputs next week, as they offer the first timely read on how confidence, pricing pressure and hiring intentions are responding to the Iran conflict. Global S&P PMI data already point to a broad-based deterioration in activity across both manufacturing and services in March, suggesting that sentiment has weakened quickly. On Wednesday, the ISM Manufacturing PMI for March will be released. After posting expansionary readings in January and February, the index is expected to soften but remain near the 50 threshold. Markets are not pricing in outright contraction, but any sharper than expected pullback would likely reinforce concerns about growth momentum at the end of the first quarter and early into the second quarter. Investors will be especially focused on the Prices and Employment sub-indices, as these components speak directly to margin pressure, inflation dynamics, and labor demand.

Retail and food services sales, also released on Wednesday, will be backward-looking but still relevant for market narratives around the consumer. The February data will not reflect the Iran conflict, yet January’s weak reading already raised questions about household momentum. Consensus expects some rebound in February, which would help stabilize sentiment in the near term. That said, markets are likely to look through the February figure and focus more on the implications for March and beyond, where higher gasoline prices pose a clearer threat to real purchasing power.

Labor market data will also be closely watched for confirmation that employment growth is slowing without collapsing. The ADP employment survey is expected to show an increase of roughly 40,000 private sector jobs in March, ahead of Friday’s non-farm payrolls report. February once again highlighted the monthly divergence between the ADP and the Establishment Survey prints, underscoring the uncertainty markets face when interpreting near-term labor signals.

On Friday, the non-farm payrolls report is expected to show job growth of about 50,000. While this would mark a partial recovery from February’s negative print, it would still be consistent with a cooling labor market. For markets, this combination – slower job growth but no sharp deterioration – would likely reinforce expectations that the labor market is decelerating in an orderly fashion rather than signaling a recession. The ongoing adjustment to AI adoption, combined with caution stemming from geopolitical uncertainty, suggests firms remain reluctant to meaningfully expand payrolls.

Finally, the ISM Services PMI, also released on Friday, will be particularly important given the service sector’s dominant role in US growth. The index has remained firmly in expansion in recent months, supporting the notion of economic resilience. A modest pullback in March would not, by itself, unsettle markets, but a sharper move – especially in the prices or employment components – could heighten concerns that higher energy costs are beginning to weigh on demand and margins.

In sum, next week’s data flow arrives at a sensitive moment for markets. While none of the releases alone is likely to be decisive, together they will shape expectations around growth, inflation and the labor market at the end of the first quarter and as we enter the second quarter. Most importantly, they will offer the first concrete evidence of how the Iran conflict is filtering through to economic behavior and, by extension, to market pricing.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.